Where’s Canada in the 2025 Art Basel and UBS Art Market Report?

Thoughts on what the Art Basel and UBS Art Market Report 2025 says, and doesn’t say, about Canada’s place in the art market.

The Art Basel and UBS Art Market Report 2025 by Arts Economics was released this month. As you might expect, the art market has contracted. Private sales and auction results have declined globally. This isn’t surprising given rising global trade conflicts and the trajectory already laid out in 2023. The 2020 pandemic bottoming out was followed by a strong post-pandemic recovery that saw new collectors and new ways of collecting come to market. This brought both energy and volatility to the market. 2023 and 2024 saw a significant thinning out of the high-end market, but a surge in lower end sales volume (few were buying a $3 million Old Master oil painting, but many were buying a $5000 silkscreen or photograph).

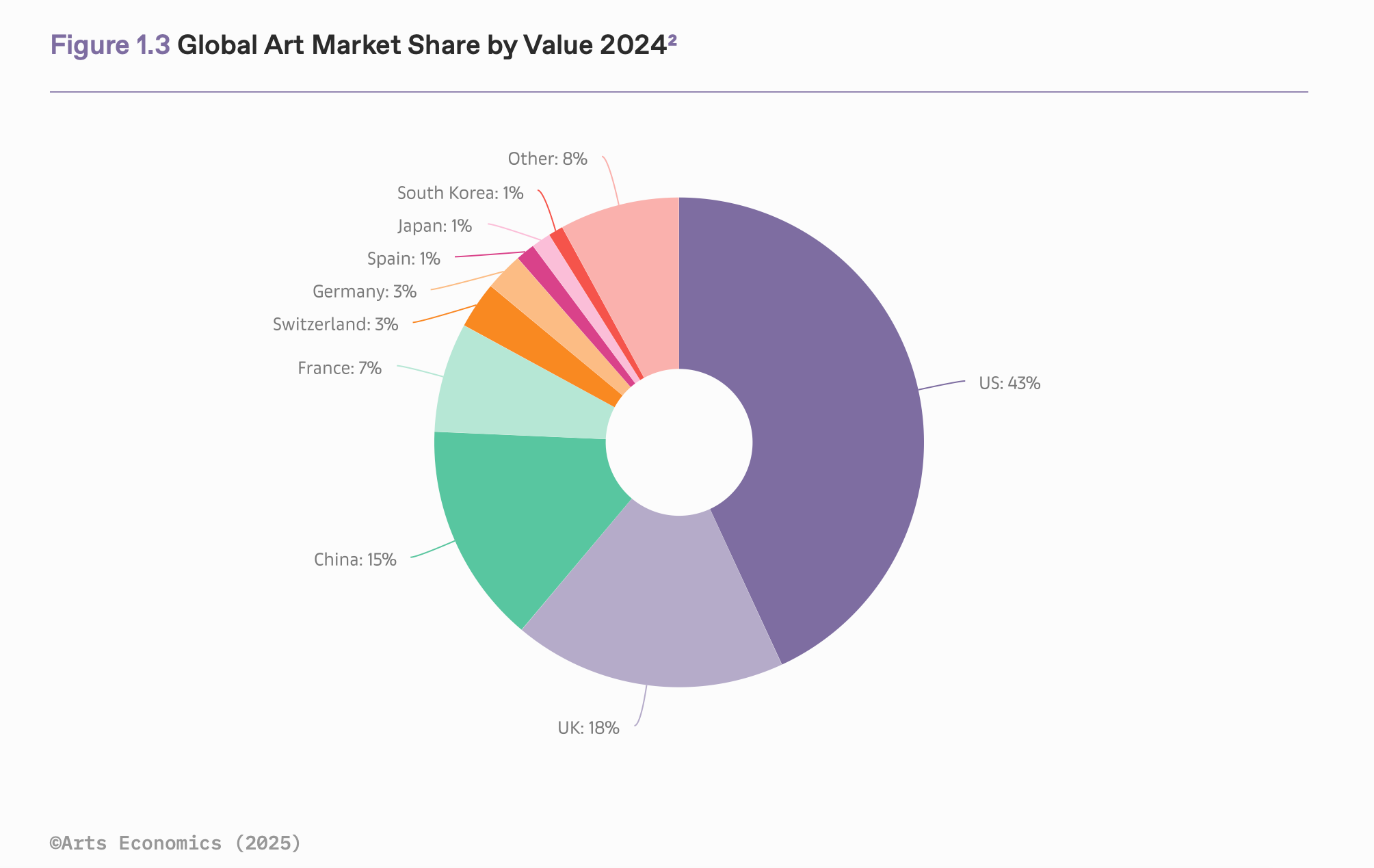

The Art Basel and UBS Art Market Report focuses on the big markets of the United States, the UK, and China, and also on the top-tier auctions houses such as Sotheby’s, Bonhams, and Phillips. But do these statistics from the art market’s major players line up with what we see in Canada? And, what do they suggest we might anticipate in Canada as we move through 2025?

Let’s take some of the key themes and indicators in this 264-page report (which I have read so you don’t have to, though I recommend you do) in stride.

High and Low Ends of the Market

While there were still multimillion-dollar sales occurring worldwide, supply at the high end was significantly tighter, with more activity and growth in lower-priced segments. (20)

As in all other years, most of the transactions carried out at auction houses in 2024 were at the lower-priced end of the market, with 95% of individual lots sold priced at less than $50,000, up by 2% year-on-year. (177)

This trend strongly aligns with Canadian market behavior, but not necessarily for the same reasons. It is not typical that Canadian top-tier auction houses like Waddington’s, Cowley Abbott, or Heffel bring to market major international Old Master works. You’re not going to see a $22 million Titian at a Canadian auction—and there’s no expectation you should. If someone wants a Titian, they’ll go to international auction houses. So, what does the Canadian top-tier look like? Well, very Canadian: a $5.7 million Jean Paul Riopelle from Heffel or a $1.8 million Lawren Harris from Cowley Abbott. These auction houses do sell international art successfully, though it typically tends to stay in the low-million dollar range and tends to fall into Post-War/20th Century instead of Old Master like Cowley Abbott’s Andy Warhol portraits of Queen Elizabeth, which sold just under $1 million.

The reason the trend aligns but not necessarily for the same reason is the ultra-high end of the art market simply does not exist in the same way in Canada. Auction houses here know this and take advantage of this fact. Waddington’s summary of their first six months of sales in 2024 list a flurry of significant sales of international art but generally in the $15,000-35,000 range. Other top-tier Canadian auction houses report similar successes. This lower-end dominance is evident in Canada perhaps in part because of these global trends pointed to by the Basel USB Report, but also more likely because the market has always trended that way in Canada. Even when we look to more regional auction houses such as Levi’s Auctions in Calgary, which specializes in Western Canadian artists, they often see the majority of works sold under $5,000, especially for contemporary or local pieces.

Online Sales

Online sales declined by 11% to $10.5 billion in 2024, lower than the last four years but still 76% above pre-pandemic 2019. The share of e-commerce out of total art market sales was stable year-on-year at 18%. (18)

Surveys of HNWIs carried out in 2024 by Arts Economics and UBS, with responses from over 3,660 art buyers in 14 global markets, revealed that most respondents preferred to buy from a dealer, but when doing so, just over half (52%) preferred buying via their websites or social media channels and without viewing the work in person (versus only 30% in 2023 and 37% in 2022). (33)

Heffel has reported that “2024 was remarkable for our online auctions.” This aligns with the global trend of collectors becoming more comfortable buying art sight unseen. Heffel's implementation of digital documentation, such as high-resolution images, detailed condition reports, and even in-gallery images using people for scale, provides buyers with a level of digital confidence. Other auction houses have made a similar shift with Cowley Abbott and Waddington’s shifting towards hybrid models that combine live previews with digital auctions, offering the tactile experience of viewing art in person with the convenience of online bidding.

In the field of private sales, this is somewhat old hat. The use of Instagram by galleries such as Patel Brown Gallery and Blouin Division exemplifies the growing trend of leveraging social media for art sales. These platforms allow galleries to showcase artworks to a broader audience, engage with potential buyers directly, and facilitate sales without the need for physical interaction. This strategy is especially appealing to younger collectors who’d rather scroll than call.

Online sales have become the post-pandemic norm, but it’s worth asking in a country where major cities are hours apart from one another, if the e-commerce approach will face a similar decline as outlined by the Basel USB Report? In Canada, I wouldn’t count on it.

Private Sales

In more volatile or uncertain periods when the market is perceived as being less buoyant, private sales – whether through a dealer or an auction house – have often outperformed public auctions, as sellers opt for private transactions with greater control and flexibility over pricing and schedules, while keeping the details and level of demand out of the public domain. (22)

Sales in the dealer sector continued to show mixed results in 2024, with aggregate values declining by 6% to $34.1 billion. Reflecting the wider market trend, dealers at the highest end reported some of the largest declines in value, as transactions continued at a level pace but with most activity concentrated at relatively lower price levels. The smallest dealers with turnover of less than $250,000 reported the largest increase in sales (17%), their second year of growth and a market turnaround for this segment which had seen the weakest recovery in 2021 and 2022. (54)

In Canada, the shift toward private sales during times of market uncertainty has mirrored global tendencies. Major auction houses like Heffel and Waddington’s have increasingly promoted their private sale services in recent years, suggesting a growing demand for more controlled and non-public avenues. In periods of market hesitancy, private sales have become especially relevant at the high end of the Canadian market, where sellers of blue-chip Canadian artists such as Emily Carr, Lawren Harris, and Jean Paul Riopelle are often reluctant to risk works not meeting their reserve at public auction. Cowley Abbott, for example, operates private sales with Ohler’s Fine Art offering a range of Canadian works of this ilk.

In line with the Basel USB Report’s observation about small dealers seeing a growth resurgence, Canada’s sector of art dealers seems to be carrying on with success. Unlike auction houses, records of private sales are not made public and so determining how these galleries are doing is difficult. But, there certainly seems to be a demand for dealers focusing on emerging or lower value sales. If we look to artists as an indication of how dealers are doing, there seems to be an issue of supply (a shortage of dealers) and demand (from artists). A 2024 Hill Strategies Research Survey titled “How are Canada’s artists doing?” revealed that roughly two-thirds of responding artists selected grants and sales as important challenges and that this would be the

first challenge that they would change if they had a magic wand—a loud and clear signal for dealers to open their walls to a larger roster of artists.

With global large-scale gallery and dealer sales declining, especially for higher-end works above $500,000, the growth in sub-$250,000 turnover among smaller dealers indicates a healthy mid-market revival, good news for Canadian dealers. Many of these dealers focus on underrepresented or regional artists, often selling directly through studio visits or informal networks. I’m thinking here of the fantastic Saskatchewan Network for Art Collecting. Launched in 2012 it contains a database of over 600 biographies of Saskatchewan visual artists and acts as a switchboard connecting artists to representation to buyers. It even hosts regular auctions. Certainly places like this act as drivers of a more inclusive collecting culture, with collectors less concerned about prestige and more motivated by personal connection or cultural relevance.

And, on the high-end of private sales, there were there collectors that made the ArtNews Top 200 Collectors of 2024: Bob Rennie (Vancouver), David Thomson (Toronto), and Steven Latner and Michael Latner (Toronto). This is down from five in 2013 where the list included Ydessa Hendeles and Joey Tanenbaum. Isn’t it surprising that so many names that might come to mind aren’t on the list?

Art Fairs

The share of art fair sales over all dealers edged up slightly year-on-year, with sales at live events comprising 31% of total sales, up by 2% on 2023, although remaining lower than 2022 (at 35%). (119)

Art fairs are a good reflection of a cautious yet steady return to in-person events globally. In Canada, major art fairs like Art Toronto and Plural Montreal have mirrored this pattern, demonstrating resilience and adaptability in the post-pandemic art market landscape.

Art Toronto, Canada's largest art fair, reported over 20,000 attendees and more than $10 million in onsite sales in 2024. With over 110 exhibitors, 76% of galleries reported selling to new clients, a sign of healthy demand. Notably, 59% of the 2,200 VIP attendees, who have an average annual art spend of $35,000, purchased art either onsite or through follow-up with galleries. These figures underscore the fair's role in facilitating significant commercial activity and expanding collector bases within the Canadian art market.

Similarly, Plural Montreal, formerly known as Papier, has solidified its position as a key event in Canada's contemporary art scene. Organized by the Contemporary Art Galleries Association (AGAC), the 2025 edition of Plural welcomed 37 galleries from seven Canadian cities, showcasing works from over 500 artists. The fair's programming included panel discussions and exhibitions that highlighted the diversity and vibrancy of Canadian contemporary art.

These developments in Canada's art fairs align with the global trend of a gradual rebound in art fair sales. The sustained interest and participation in events like Art Toronto and Plural Montreal point to a Canadian art market that’s not just holding steady, but evolving alongside global shifts. As the art world navigates the balance between digital and in-person experiences, Canada's art fairs remain pivotal in fostering connections between artists, galleries, and collectors.

Trade and Tariffs

The US’s largest bilateral trade partners remain the large and mid-sized art markets in Europe, with France, the UK, and Germany accounting for 56% of imports and 41% of exports in 2024, positioning these markets as the most at risk if tariffs are raised. However, any anti-trade policies for imports or exports are potentially damaging to the US art market, which has built its leading position as a key hub for the art trade by relying on both international buyers and sellers of art to complement its sizeable domestic base. (25)

As of March 2025, UBS did not expect US tariffs on Canada and Mexico to be sustained, although the bank noted a greater risk that highly aggressive tariffs and retaliatory measures will remain in force long enough to weigh on the global economy, lowering their forecasts for a benign tariff scenario and increasing their odds of a highly aggressive tariff scenario from 25% to 35%. (38)

This part is still unfolding, and only time will tell how it affects Canada. Notably, the Basel USB Report highlights the United States' reliance on international trade, particularly with European partners, to maintain its dominant position in the global art market. Of course, recent developments in United States trade policy, notably the imposition of a 25% tariff on Canadian art imports, have introduced significant challenges for the Canadian art market.

Canadian galleries and collectors are already feeling the impact of these tariffs. For instance, Stephen Bulger, a Toronto-based dealer, canceled plans to exhibit an artist at the AIPAD fair in New York as a result of the strain and uncertainty imposed by the tariffs, which, by the way, would have increased the cost of participation by 25%. Additionally, the Art Gallery of Ontario expedited $1million in purchases from United States galleries during the 30-day pause in tariffs, indicating a shift in acquisition strategies.

In response to these challenges, Canadian art institutions and dealers are seeking to diversify their markets. Art Toronto, the country's largest art fair, is expanding its outreach beyond the United States, engaging with European and Asian markets. In an Art Newspaper interview with the fair’s director Mia Nielsen she says that “We are expanding our gallery outreach efforts beyond the US market. For 2025 we’re working with a UK-based curator to deepen ties to the European scene, as well as Asia and South America. We’ll see in October if this strategic pivot actually reduces dependency on the United States market and provides new opportunities for Canadian artists and galleries.

The current trade tensions underscore the importance of international collaboration and open markets in the art industry. It appears that any disruption to global trade, whether due to tariffs, inflation, or logistics, would disproportionately affect Canada’s smaller dealers and artist-run spaces, many of whom rely on a stable and supported arts market for long-term sustainability. While Canada’s domestic collector base is growing, it is still limited in size and concentration, with most high-value private sales focused in Toronto, Vancouver, and Montreal. As Canada navigates these challenges, the resilience and adaptability of its art market will be crucial in sustaining growth and fostering global connections.

And in the end…

If one thing is clear from this year’s Art Basel and UBS Report, it’s that no market is immune to the pressures of geopolitics, changing technologies, or collector behavior. But Canada has never quite played by the same rules as the global giants, and that might actually be its strength. Our market isn’t top-heavy, nor is it overly reliant on any single channel.

As we move further into 2025, Canada’s art market continues to show signs of resilience. While global trends like a thinning high-end and a booming lower-end resonate here, Canada’s unique collector culture, regional diversity, and appetite for both online and private sales position it well for continued, if modest, growth. The key will be adaptability: for galleries, artists, and institutions alike. Whether it's through strategic shifts in trade outreach, embracing digital tools, or supporting more inclusive dealer networks, Canada’s art scene is evolving in a way that deserves close attention—and perhaps, a bit more optimism than you might expect from the headlines.

So what does all this mean for you as a collector, artist, institution or curious observer in Canada? It means that while the big reports give us helpful global context, the real story is still local. The Canadian art market doesn’t just follow global trends—it filters them, adapts them, and sometimes quietly resists them.